Last year I wrote about my initial impression of goPeer, a Canadian peer-to-peer lending service. I even wrote a goPeer Investment Calculator to help calculate the potential earnings. If you have not heard about it I highly recommend checking it out, either as an investor or as a borrower.

I dabble in all sorts of self-directed investing mechanisms including traditional stocks,covered call ETFs, real estate investing platforms like Addy. It’s no surprise that the past year has been a tough year for Canadians not only to buy basic goods such as food and gas, and to pay rent. Inflation due to war, greedflation, excuseflation, and supply chain troubles continue to eat away at our retirement savings. That’s why I’m glad to share some good news:

I’m a data nerd, every month I take a snapshot of my financial situation. I’ve been doing this monthly for several years and I’ve found it very useful. It helps me take stock of what I need to change, what’s working and what’s not. I keep it super simple, for every investment, asset and liability I have they are represented as a column in a simple spreadsheet that I update once per month. Here’s a fictional example:

Month

Cash

TFSA

RRSP

GoPeer

Addy

2023-01-01

10,000

45,000

45,000

10,000

7000

2023-02-01

10,300

44,000

46,000

10,100

7000

2023-03-01

10,220

47,000

47,000

10,200

7000

2023-04-01

12,000

48,000

48,000

10,300

7050

And every year usually around tax time I review how the year went and plan for the next:

How much should I try to save for the kids RESP?

How much should I try to put into TFSA?

Should I max out RRSP contributions?

I also review the overall performance of each investment:

Is this still the right risk profile for this stage of my life?

Is it doing well? Should I change anything?

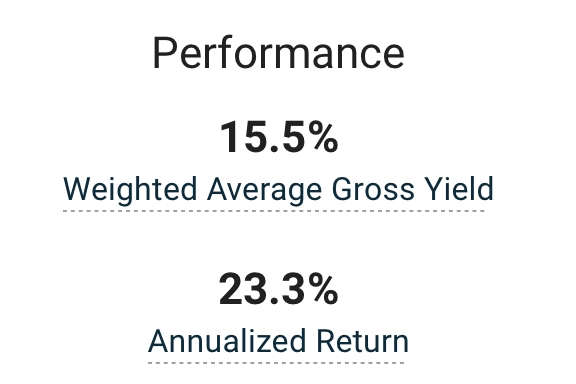

That’s when I was surprised to discover that goPeer was the best performer across all my investments this year!

goPeer was the best performer across all my investments this year

Here’s a screenshot of my rate of return:

And this is not just me, I’ve found other goPeer users who are posting far better rates of return than what I have been able to make, here are some screenshots from them that were posted on the Addy discord, a chatroom where Addy users hang out:

That said, there are those that did not do as well, but still very respectable:

So I highly recommend Trying it out for yourself! Using my referral link will help us both out: you’ll get $30 bucks and I’ll get $30.

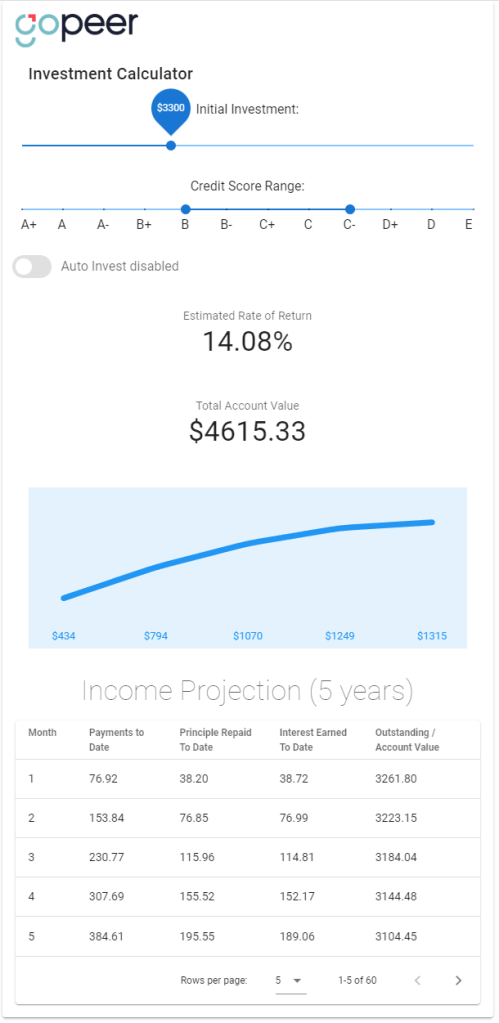

I recently blogged about my experience with goPeer so far and I’m really enjoying the service. One thing I thought it could use though is an income projection calculator. So I created one and thought I would share it. You can find it here.

How to use the calculator:

Using the initial investment slider choose the amount you would like to invest

Use the credit score slider to choose your minimum and maximum credit score range

If you are going to set your account to auto-invest, enable the auto-invest slider

Understanding the output

The tool uses the statistics published by goPeer to calculate an estimated rate of return based on the credit score range you choose. Obviously, the higher-risk loans you choose to fund increase your rate of return.

The tool outputs a Total Account Value that estimates what your total balance will be at the end of 5 years. This is because goPeer allows for 3 and 5-year repayment terms. for now, the tool just assumes that all notes are 5-year terms.

The graph projects the total interest earned at the end of each year. The table below the graph shows the monthly Payments to Date which are the cumulative total payments received, Principal Repaid to Date which is the total amount of your original investment being returned to you, the Interest Earned to Date which is the cumulative total amount of interest you have been paid and finally the Outstanding Balance or Account Value which is how much of your original investment remains to be repaid.

I hope you find it useful, and please let me know if you would like any features or enhancements in the comments below.

I recently wrote down my thoughts on buying an apartment for our children to live in while they are in university in order to save over $288,000 in rent payments. What I did not mention is that our oldest child has almost finished his first year. I thought I would take some time to share the actual costs of sending your child to university these days since a lot of the information I’ve seen is wildly inaccurate.

A couple of things to note: He is in the arts program and is interested in becoming a psychologist. He also wanted to meet others in his first year and opted to stay on campus which we highly recommend especially after the isolating past few years. He has a large group of friends who help each other out which would not have been possible if he was alone in an apartment out there (and less expensive too). We also needed to sign him up for a meal plan. By the way: he and all his friends needed to buy extra food plans as they ran out of food credits.

The Financials:

Item

Cost

Spending Money

$4,000

Tuition

$5,616.90

Food

$5,579.72

Other School Expenses (Books, Fees, Etc)

$1,449.38

Housing

$7,719.00

Total

$24,365

To date, we’ve withdrawn $20,365 from his RESP to pay the bills and we’ve given him around $4000 for other expenses throughout the year.

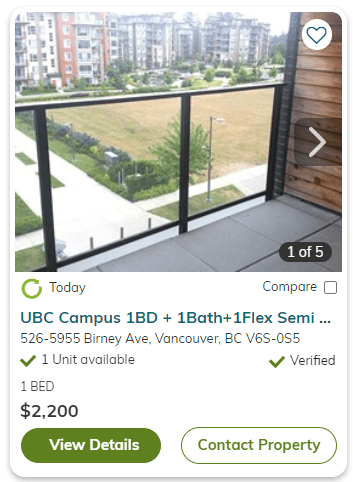

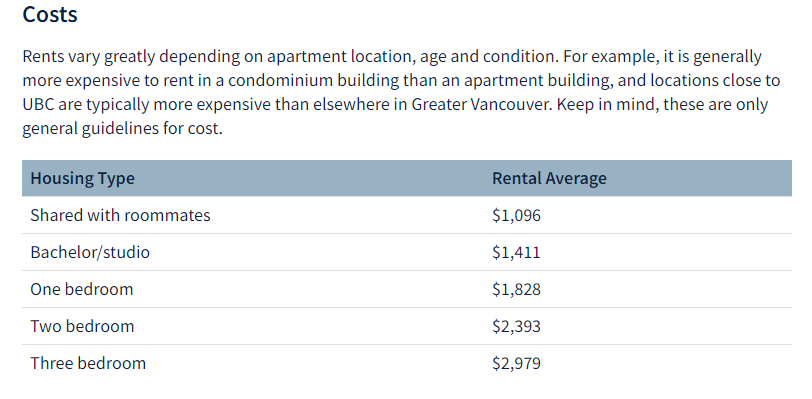

I have 4 boys, and they all want to go to the University of British Columbia (UBC). The University is too far from home to travel back and forth so they will need to stay on campus. So let’s do a quick search to see what it would cost to rent a 1 bedroom apartment close to UBC:

Woah. Alright, let’s do some simple math. how much is this going to cost us? Before we run the numbers let’s make a simple assumption that each kid will spend 48 months in university (based on this). Also, it turns out that I will have 2 kids in university at a time which makes things easier. The math: 4 kids * ($2,200 per month x 48 months) = $422,400

That can’t be right, can it? I dug into the rental costs a bit deeper and grabbed this right off the UBC website:

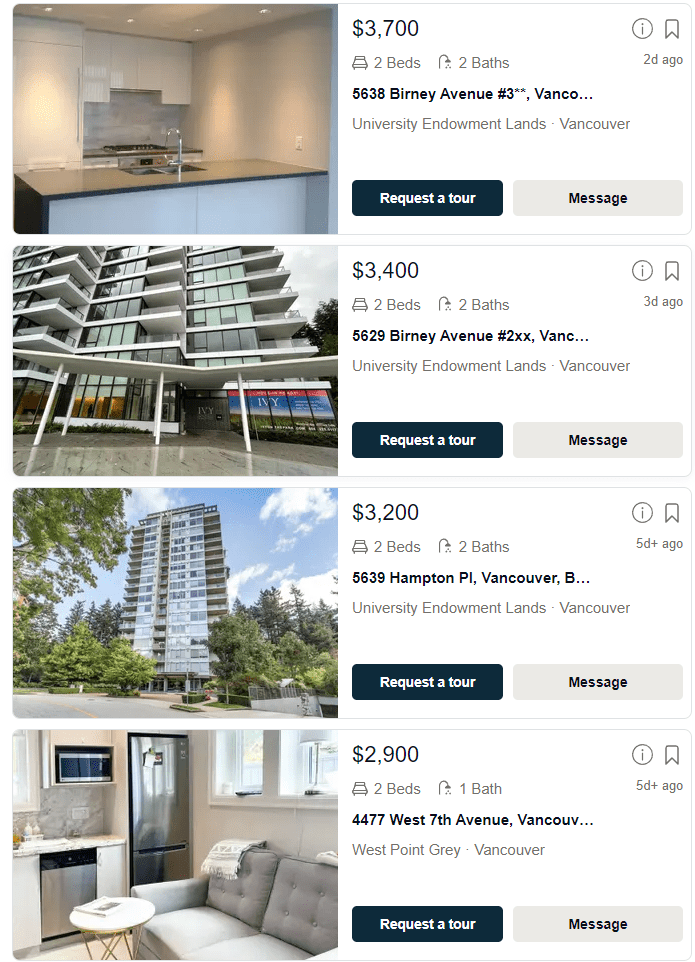

OK, that’s better: assuming two kids going at the same time a 2 bedroom should lower the cost to 4 kids * ($1,196.5 per month x 48 months) = $229,728. But in reality, I could not find anything that cheap. So Let’s split the difference and say close to $1,500 per month per kid or $288,000 total cost using the same math as before. Here’s a sample of what 2 bedroom apartments are going for around UBC:

Should I buy an apartment?

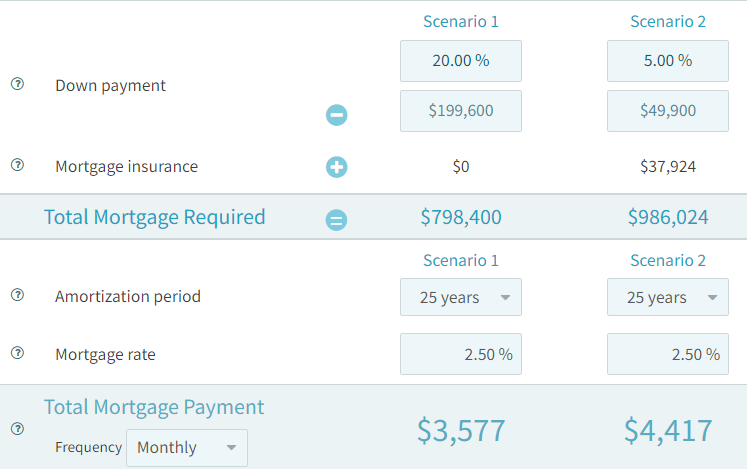

Wasting more than a quarter-million dollars renting does not sound like a good idea, what if I just bought an apartment for ~8 years and sold it once the boys are out of university? A quick search shows I could get a 2 bedroom 2 bathroom for $850 – $1 Million.

Let’s run some math on that place on Berton for $998,000 then:

Let’s take two different approaches here. In Canada, you must put 20% of the purchase price as a down payment, Let’s call that scenario 1. For down payments of less than 20%, home buyers are required to purchase mortgage default insurance, commonly referred to as CMHC insurance. let’s call that scenario 2. Here’s what the numbers boil down to assuming a 2.5% interest rate:

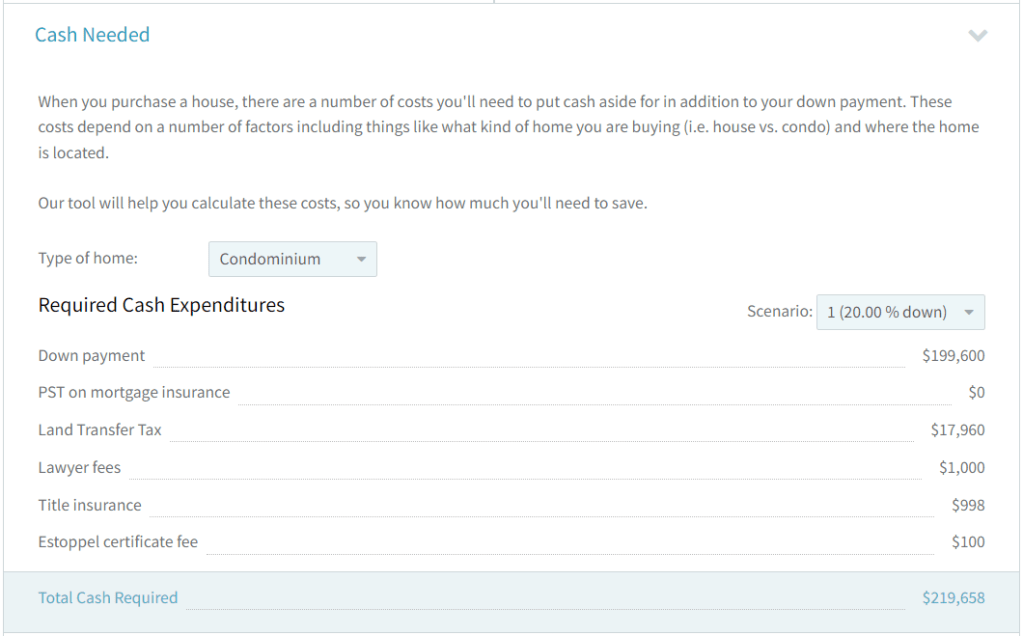

OK, so we can see that we are a bit higher than what it costs to rent but not by too much. Let’s look at total cash upfront requirements for both scenarios:

Scenario 1:

And scenario 2:

Now let’s calculate the total cost of having the apartments across the 8 years in all scenarios:

Item

Scenario 1: More upfront

Scenario 2: Minimal upfront

Scenario 3: Just Rent

Upfront Cash

$219,658

$69,958

$0

Maintenance fees

$40,762

$40,762

$0

Total Payments

$343,392

$424,032

$288,000

Grand Total

$603,812

$534,752

$288,000

Phew, so the cost of ownership is almost twice the cost of renting. But, of course, after the 8 years is up we can either sell the apartment or rent it out to other students. Let’s project a couple different scenarios for how much our apartment would appreciate over 8 years: none, 20%, 40% and 60%.

Scenario 1: More upfront

No Appreciation

20% Appreciation

40%Appreciation

60%Appreciation

Sale Price

$998,000

$1,187,600

$1,397,200

$1,596,800

Mortgage Balance

$593,952

$593,952

$593,952

$593,952

Payments Made

$603,812

$603,812

$603,812

$603,812

Profit

-$199,764

-$10,164

$199,436

$399,036

Scenario 2: Minimum upfront

No Appreciation

20% Appreciation

40%Appreciation

60%Appreciation

Sale Price

$998,000

$1,187,600

$1,397,200

$1,596,800

Mortgage Balance

$687,267

$687,267

$687,267

$687,267

Payments Made

$534,752

$534,752

$534,752

$534,752

Profit

-$224,019

– $34,419

$175,181

$374,781

My sister-in-law is a realtor and was able to look up the sales history of this apartment. It sold in 2016 for $800,000. If we purchase at a list price of $998,000, the current owner will see an appreciation of 24.5% over 6 years or 4% per year. Assuming the same rate of appreciation over the next 8 years we could sell the apartment for $1,317,360 and realize a total profit of $95,341.

Scenario 3: The DormApproach

Another approach (if you can get in) is renting a room in a dorm. A connected single room in orchard commons (a pretty nice place) which is a private bedroom and shared bathroom is $13,298 for the year (you need to include the meal plan). If all 4 boys go this route for 4 years each we are looking at $53,192 per student or $212,768 total. But I hear that students have a tough time living dorm life after the first or second year.

Other Costs

Before you grab your pitchforks: I realize I left out property taxes, apartment insurance, the potential rise in apartment rental fees, and probably a few other things. Property taxes would probably total around $20,000 and insurance around $4000 which is pretty close to the cost of rental fee increases so I decided to cancel them out for the sake of simplicity. If you disagree or think I left anything major out let me know and I’ll update the post.

Summary

So it’s quite clear that even with the insane cost of housing these days owning is better than renting but not nearly as good as I thought it would be. I think what I’m going to do is have the kids use student loans to pay their fair share of the rent, then, each dollar they pay will be a share of the total ownership of the property. This way we all win down the road, either we sell and they pay off their student loans right away or we rent it out and pay them off over the long haul. I’d love to hear your thoughts and what you might do differently.

I spent the majority of my adult life programming software and leading teams. In software development, A team or department will usually consist of product managers, user experience designers, software engineers, devops engineers, engineering managers, project managers and the list goes on. Each role is there to ensure that the product produced best meets the needs of the customer. But this all happens after you already know what the product is that you are building.

The new Molecular Beverage Printer by Cana

Before all this, all you have is an idea. Maybe you want to build the world’s first molecular beverage printer or the first personal electric aerial vehicle. In one’s mind it’s probably a foregone conclusion that of course, the world needs this product. I mean heck, why wouldn’t they? But the truth is that most ideas fail even if executed competently. I think the figure is actually north of 80% but honestly, the stakes are so high that even if the failure rate was 20% it’s worth understanding how to reduce that margin for failure as much as possible before investing more time and money into any idea.

Software engineers often get an idea and immediately crack open their favourite coding tools and whip up prototypes: Simple, crude versions of the idea that mostly work but might be lacking features or functionality but are usually enough to get the point across. And, as I’ve witnessed many times in my career code wins arguments. Having a working mobile app, website, API, game or whatever takes the guesswork away. The conversations become more practical and less hand-wavy. Prototypes are great.

But, sometimes the idea is not something that is easy to prototype. Let’s take the molecular beverage printer example above. I’m pretty sure prototyping a machine like that would be no simple feat. So how then could you determine if the market would be ready for a product like Cana without building the beverage printer first? This is where pretotyping and “the right it” by Alberto Savoia comes in.

To give you an example of how we might approach pretotyping the molecular beverage printer let’s use what Savoia calls The Relabel Pretotype. This is where we might take an existing product and simply by re-labelling it, we can test whether our customers might buy. In our case, we might take a bevi (a fairly similar machine that uses traditional syrups) and just put a different skin on the front and plop it into a beverage trade show floor.

Sure, you might not be proving the taste of the molecularly printed beverage meets the quality bar that the consumer demands but you will gather a lot of your own what Savioa calls YODA (Your Own DAta) . You’ll learn whether the market is even ready to drink a molecularly printed beverage on premise alone. You’ll learn where your target market might be, airplanes come to mind since they are weight and space constrained and god it would be great to have a nice whiskey sour on my next trip to SF.

I thoroughly enjoyed the book and if you pick it up on amazon please use this link. It will help me cover the costs of running this site.

p.s. If anyone wants to take a stab at how one might pretotype a personal flying machine let me know in the comments. 😉

Lately, I’ve been trying out different passive investing services as part of my goal to generate enough passive income to live comfortably. In a recent post I talked about my experience with goPeer, a peer-to-peer lending service that is a great way to earn passive income. In this post, I’ll share my experience with Addy, a real estate investing service. There are many of these types of services in the U.S.A. but not many in Canada so I thought I would share what I’ve learned.

What’s Addy?

Addy is a real estate investing platform that aims to make real estate investing possible for everyone. Addy’s professional team identifies the real estate investment opportunities and does all the heavy lifting for you. You can invest as little as $1 and own a share (called units) in a boutique hotel in Montreal or campground in Lakefield. Super cool! Many of the investment opportunities offer a projected return of 12% or more.

How it works

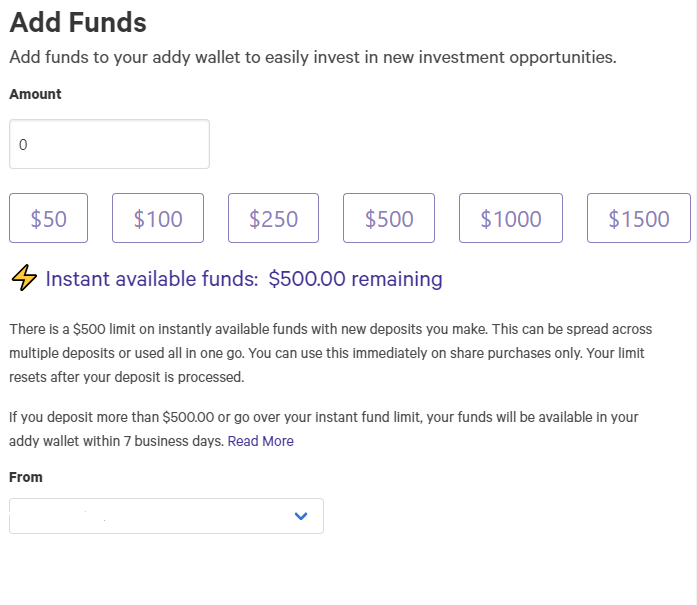

First, you’ll need to sign-up for a membership which is $25 per year for a basic or $500 for a 5-year membership which comes with some extra benefits. I think they should do away with the membership fee upsell you once you’ve got past your first investment but that’s just me.

Then you will need to connect your bank account to transfer funds into your Addy wallet. This was a major sticking point for me as I’m super nervous about connecting my account so I spent a bunch of time reading up on the owners of the business, where they are located, background etc.

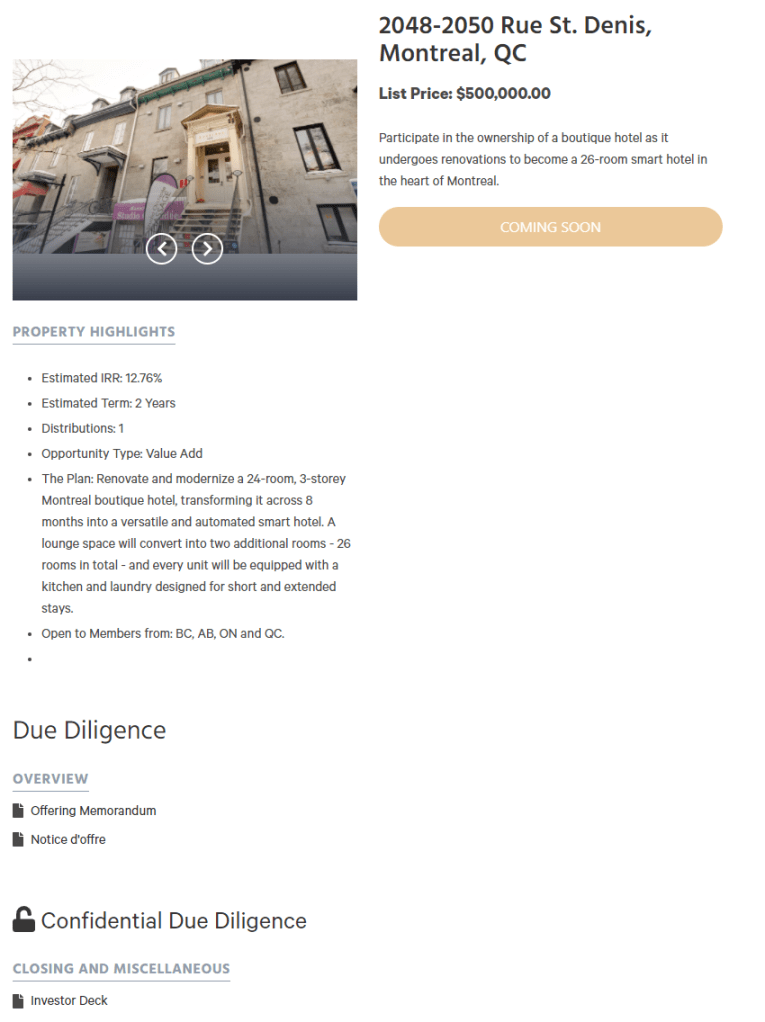

With the formalities out of the way, you will be presented with a dashboard with the usual suspects: your wallet balance, total investment, new properties etc. The property view looks like this:

From this screen, you can read more about the offer, dig into the Offering Memorandum, flip through the investor deck and if you so choose – invest in the property.

What I like (so far)

What I like so far about Addy is that you are not swamped with tons of properties to invest in and left to your own devices. Addy seems to carefully plan out each property and presents you with videos, slideshow presentations and even honest pros and cons videos. I honestly feel like I can make a fairly well-informed decision especially if I take my time to read through the very detailed offering memorandum – a 50-page document outlining all the plans, financials and potential returns.

There is something about Addy that just feels good. When I invest with Addy I feel like I’m investing in my community, city, country. Many of the projects are turning run-down buildings into low-cost rent or revitalizing an area.

So far I’ve only invested $2500 into a few properties and since my investments won’t pay off for some time I’ll probably be blogging more about my experience down the road.

If you like this summary and want to give Addy a try, please use this link. we’ll both get $25 bucks to invest in our next property!

One of my life goals is to generate enough passive income to live comfortably. One of the ways to generate more passive income is by taking part in a relatively newer approach to lending called peer-to-peer lending.

How it works:

As a borrower, goPeer makes it very easy to apply for a loan from the comfort of your home. You need to be 18 or older, have a credit score of at least 600 and have a regular source of income over $15k per year. Aside from that you must be a Canadian and have a Canadian bank account.

As a lender, after you sign up, you will be asked a few questions about your investment goals. Then you will be asked to connect your bank account to transfer funds into goPeer. This was the most stressful part for me. I actually wimped out a few times and decided to read more about the company and try again. I’m pretty comfortable having my money with goPeer so far. Depending on the loans you invest in you can expect Gross returns from 7.5% to 28%.

What to expect:

When you start using goPeer you will need to transfer some funds into the platform which can take about 5 days. I was pretty excited to use the platform and found myself logging in every day after my initial deposit to see if my funds were available to invest.

Once your funds are available you can start investing. This is easy to do. You will be presented with a screen like this which will let you pick and choose the loans you would like to invest in:

You can then drill down into each loan and view a summary of the loan details. This give’s you a simple, high-level view of the borrower’s income, the field of work, location, whether they own or rent, the purpose of the load, their credit score, debt ratio loan amount and so on. I found this very useful when I was starting out. The checkboxes indicate that goPeer has validated the information and the ‘!’ indicates they have not.

After I became more comfortable with the service I turned on the “auto-invest” feature. It’s pretty straightforward and well designed. You choose how much you want the feature to invest in each loan, select a range of credit risks and turn it on. The system will then invest into loans automatically with your settings every day.

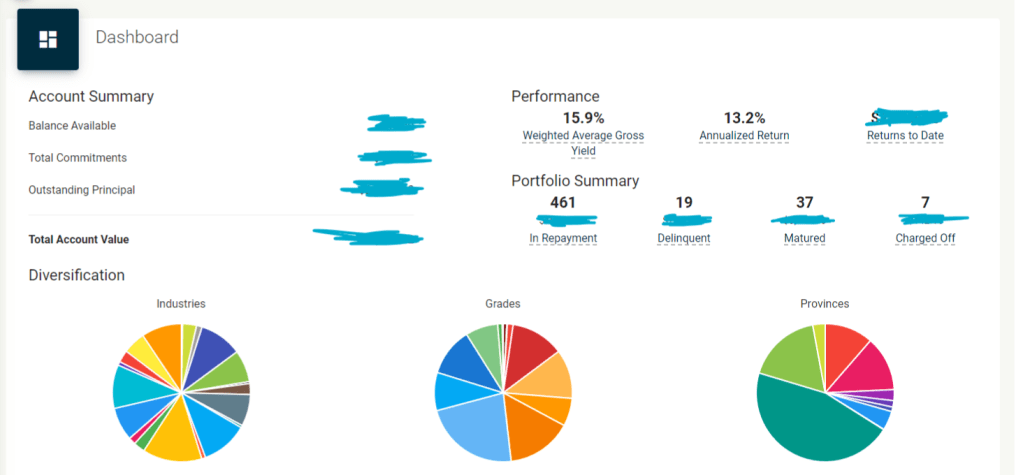

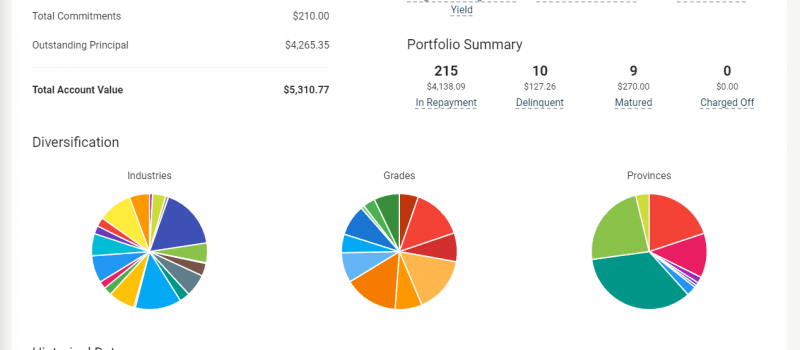

The dashboard is super clear and very user-friendly. It will give you a high-level summary of the industries, credit grades, provinces, account totals and all the high-level numbers one would expect.

I do wish they would add an income projection graph and even filed a ticket for the feature request. The support staff replied promptly, they were courteous and supportive.

goPeer says they have 4,305 investors on their platform. This is a healthy metric in my opinion because it means that you can invest a little bit into many loans on the platform which will reduce your risk of losing a bunch of money due to a borrower getting “charged out”. A term used when the borrower fails to pay their loan and is deemed unrecoverable. Everyone shares the risk.

Take your time when you start using the platform. Don’t invest too much into a single loan, spread your money around many loans and be patient. When I joined there were only a handful of loans to invest in. Avoid the temptation to overfund a loan.

goPeer also mentions that the average interest rate earned on the platform is 15.9%. That’s a pretty great return. I wish services like this existed when I was younger. The first real thing I invested in was a GIC which did not even keep up with inflation.

That’s it for now, I’ll post another update in the future with some statistics on real earnings, charge-outs etc.

Try it out for yourself! Using my referral link will help us both out: you’ll get $30 bucks and I’ll get $30.

{kind=link}